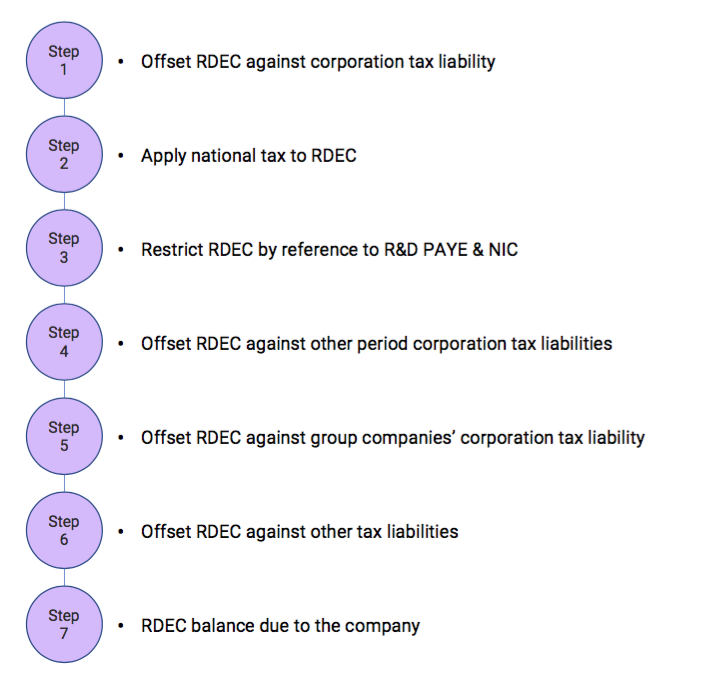

The RDEC calculation is one of the more complex areas of the R&D regime. Firstly, you have to identify the qualifying expenditure, taking care to exclude certain costs (e.g. subcontractors have different rules to the SME regime). Secondly, you must then also apply the 7 Steps of the RDEC Scheme.

The 7 Steps are found at Corporation Tax Act 2009 Chapter 6A s.104N and 104O

RDEC Calculation Example

Lets work the following scenario – Company A Ltd has

- £1m accounting profit before R&D costs

- £100,000 R&D costs

- £40,000 PAYE costs relating to R&D

- £500,000 corporate tax loss

- No outstanding other tax liabilities

- RDEC rate is assumed to be at 12%

Step 1

Offset the RDEC credit against the company’s tax liability.

If there is any RDEC credit left over, i.e there were not enough profits or the company had losses then carry the balance to step 2.

- RDEC credit £100,000 x 12% = £12,000. No tax liability so all of the £12,000 carries forward to Step 2.

Step 2

This step ensures that loss making companies receive the same net benefit as profit making companies.

This is achieved by applying a ‘notional tax’. The total cash benefit received by either profitable or loss making companies will be the RDEC value less the main rate of corporation tax, currently 19%.

The ‘notional tax’ retained under this step is carried forward to reduce the corporation tax liability of a future accounting period.

- RDEC £12,000 x (100%-19%) = £9,720 credit carried to Step 3.

- £2,280 carried forward to reduce future corporation tax liabilities.

Step 3

This step restricts the payable amount to the company’s total expenditure on R&D workers’ PAYE and NIC for the accounting period.

If the RDEC amount exceeds the PAYE/NIC cap, the difference is carried forward and added to the expenditure for use against future accounting periods.

If the RDEC amount is lower than the PAYE/NIC cap, then proceed to Step 4.

- RDEC £9,720 < PAYE £40,000. So carry forward RDEC £9,720.

Step 4

Any amount of RDEC remaining after Step 3 is to be set against any outstanding corporation tax liabilities of the company for any other accounting periods. There is no priority order over which years to offset against first, the company may decide.

- No outstanding liabilities so carry forward to Step 5 RDEC £9,720.

Step 5

If the company is a member of a group, it may surrender the whole or any part of the amount remaining after step 4 to any other member of the group.

A company can choose not to surrender to a group company, in this case the amount will be carried forward and subjected to Steps 6 and 7.

- No Group relief so carry forward to Step 6 RDEC £9,720

Step 6

Any amount remaining after Step 5 is used to discharge any other liabilities of the company. For example, VAT arrears.

- No other liabilities to pay so carry forward to Step 6 RDEC £9,720

Step 7

The final amount remaining after Step 6 is payable to the company on the proviso the conditions of s104S are met, e.g. the company is a going concern.

- RDEC of £9,720 payable to the company.